This week Carbon Re released its 'Three technologies to reduce climate change' white paper that provides recommendations to plant owners to reduce energy consumption. While there is good news in that Carbon Re identifies 13 technologies that can make a combined impact on cement plant decarbonisation to reduce global CO2 emissions by 0.8Gta in the next decade, it will rely on policymakers and outside investment to achieve such significant reductions.

Over 80 per cent of the savings can be made by 2030 with technologies are well known to the cement sector: substitution of clinker with supplementary cementitious materials (SCMs), including limestone calcined clay cement (LC3) cement, the use of biomass and waste alternative fuels (AFs), and artificial intelligence (AI) to improve energy efficiency and SCM blending.

However, the report stresses that “achieving reductions by 2030 will be more important that achieving net zero in 2050.” This statement follows research by Nature (Sun et al, 2021) that making reductions before 2030 will lead to a significantly better result than hitting net zero between 2040-50 through a big improvement.

High potential technologies

The 13 technologies that cement producers can benefit from right now can be grouped in three areas. SCMs, artificial intelligence to support SCMs, and LC3 are key in reducing the use of clinker and its related CO2 emissions. In addition, the production process can be improved through the use of AFs such as biomass, RDF and MSW, new kilns using green hydrogen or electrification, AI to improve energy and fuel efficiency, waste heat recovery (WHR), CCUS (including oxyfuel/ direct separation/ mineralisation technologies), and calcium looping CCUS. Finally, the use of graphene can help the construction industry to reduce its use of concrete.

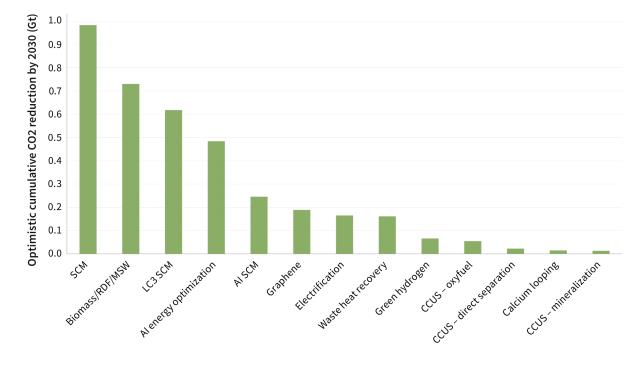

Cumulative CO2 reduction from 2023 to 2030 (Gt) in the ‘optimistic’ scenario

Of these technologies SCMs, biomass/waste fuel and AI are seen as having the biggest impact on decarbonisation for cement production by 2030, according to Carbon Re. SCMs offer almost 1Gt of CO2 reduction between 2023-30, followed by biomass and waste fuels adding a further 0.7Gt of reductions. These two technologies are expected to be joined by the LC3-type SCMs and AI by 2030. In terms of annual performance, achieving all the combined savings from the technologies listed would result in emissions being reduced from 2.5Gt of CO2 in 2022 to 1.7Gt of CO2 in 2030, a 34 per cent fall. Moreover, the technologies cited to have the most impact are the three considered to be the easiest today to adopt.

Barriers to implementation

From its modelling, Carbon Re has listed nine barriers to the success of meeting this most optimistic scenario for decarbonisation. These include the commercial interests of cement companies, the focus on 2050 technology undermining drive for change today, low market demand for low-carbon cement, cement quality and specification regulations, availability of finance for capital investment, upscaling not matching pilot plant performance, the industry's definition or perception of 'carbon neutral', and competition for scarce resources such as renewable electricity, green hydrogen, SCMs and biomass.

Long-term potential of technologies

As for long-term potential of the technologies, oxyfuel, CCUS, graphene and LC3 are detailed as having ‘the greatest long-term potential’ for decarbonising the cement sector. Financial barriers are the biggest threat to CCUS-based technologies and WHR has limited upside potential, the report concludes. Moreover, “biomass and green hydrogen-based technologies should be approached with caution,” says Carbon Re. Biomass is a significant factor in deforestation and global shipments contribute to carbon emissions. Green hydrogen requires capital investment in new kilns, a significant increase in the availability of electricity as well as an increase in the hydrogen production capacity through electrolysis. In addition, other industries will also complete for green hydrogen, leading to price increases.

Capital and operating costs

Technologies considered to be low cost and with the highest cost savings are LC3, followed by SCM (without AI), AI and SCM, and WHR. AI energy optimisation offers savings in terms of both capital and operating costs. All CCUS technologies and electrification are at the other end of the scale with high capital and operating expenditure.

Recommendations

Carbon Re makes specific recommendations from its modelling. Standard and LC3 SCMs, biomass and waste-derived alternative fuels, and AI if implemented now could deliver 81 per cent of the total 3.8Gt CO2 savings.

In terms of policy-making, the free carbon credit allowance under the EU Emissions Trading Scheme (EU-ETS) will need recalculating or removing through the introduction of the Carbon Border Adjustment Mechanism (CBAM). In addition, demand has to be established for low-carbon cements and a price premium via the public procurement process. A certification process for the carbon content of cement will also need to be established. Carbon Re also advocates a shift from ‘prescriptive’ to ‘performance-based’ standards to enable SCMs to be better used.

Getting started

Carbon Re and cement manufacturing consulting firm, A3&Co®️, have joined forces to help manufacturers cut costs and accelerate cement decarbonisation. The two organisations have signed a strategic partnership agreement and plan to work together to help cement manufacturers optimise production processes to reduce operational costs and carbon emissions to otherwise unachievable levels. Carbon Re and A³&Co® will be showcasing their work at the Cemtech Middle East & Africa 2023 conference and exhibition at the Grand Hyatt Dubai on 12-15 February.