Coal prices were falling to the lower end of the US$105-125 range amid lower supply and good gas prices. Geopolitical developments in Iran and Syria saw the oil price rise but it remained between US$70-75, supported by OPED. The International Energy Agency (IEA) forecasts a surplus in the markets.

Petcoke is recovering from long-term support and Chinese buyers are returning to the market. China is reported to allow heavy industries to continue to use petcoke. While discounts are falling, petcoke still offers good value.

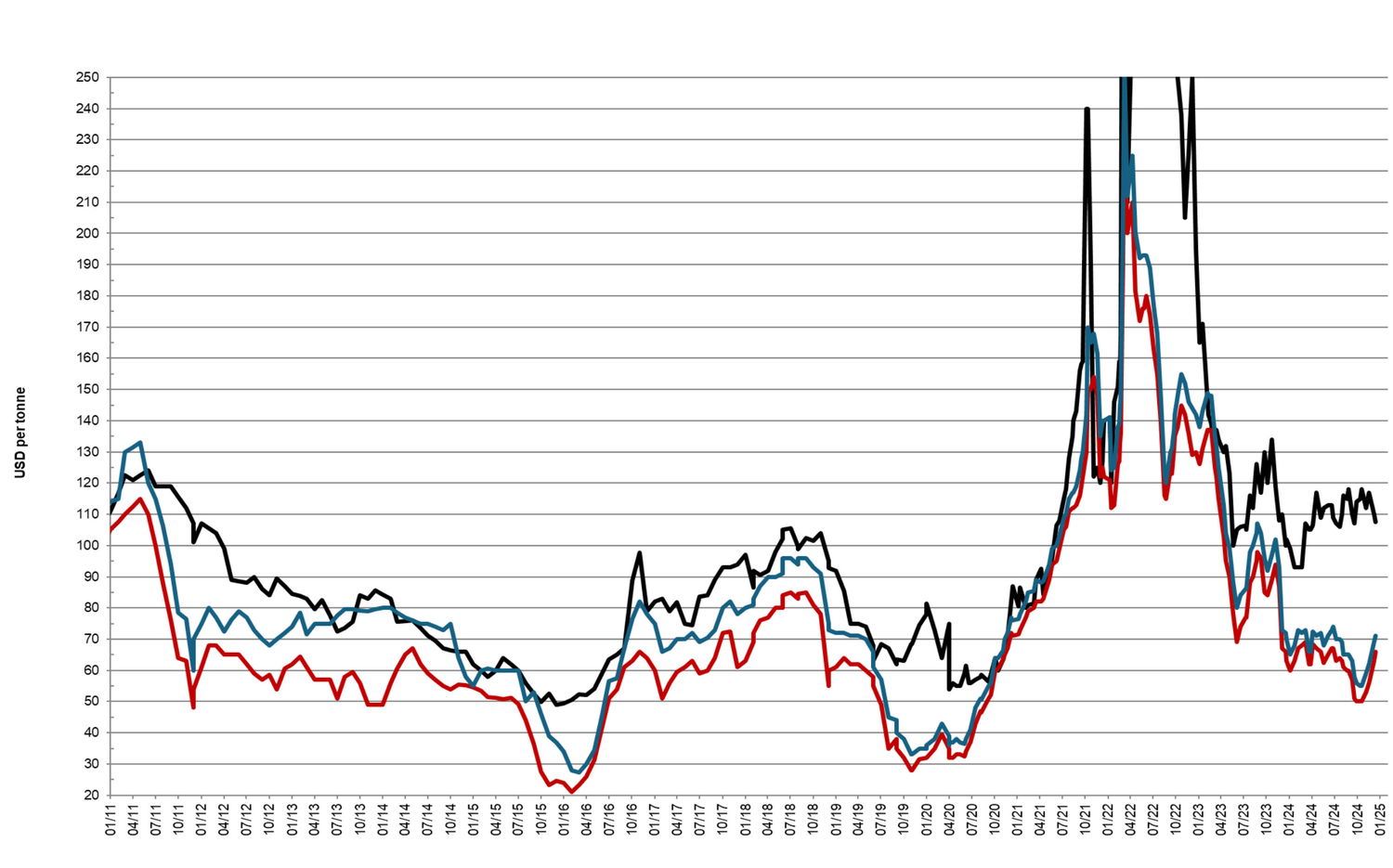

On 13 December 2024 the discount for 6.5 per cent sulphur petcoke FOB sold at US$66 is 51 per cent when compared with API4 coal sold at US$107.50 in the 4Q24. The CIF ARA 6.5 per cent petcoke contract sold at US$86.50 is at a discount of 37 per cent when compared with API2 coal sold at US$109.25 in the 4Q24.

Petcoke with 6.5 per cent S is expected to move within the US$60-70 range with resistance at US$68, US$75, US$95, US$105 and US$115. Support is at US$58, US$50, US$48 and US$40 with multi-year support at US$40. For 2025 a broad range of US$45-70 is forecast.