By Frank O. Brannvoll, Brannvoll ApS, Denmark

Since ICR’s most recent energy report, the energy complex has moved in range, awaiting the impact of sanctions on Russia and the risk of an economic slowdown.

However, the threat of EU sanctions on Russian oil pushed up oil prices in the range of US$105-120, but prices have since fallen back as high inflation and interest rate increases have sown considerable doubts on growth going forward.

Coal has been stabilising after rising demand was noted before the sanctions in August. Russia is offering a discount to non-sanction countries.

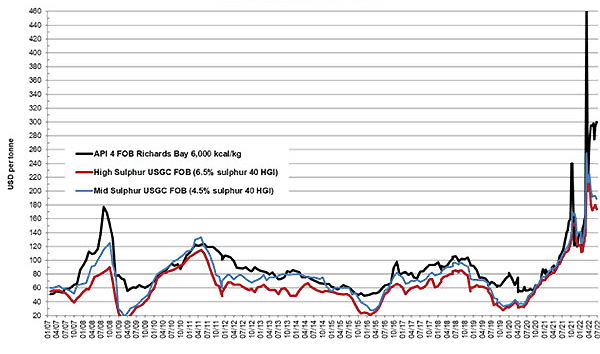

Steam coal and petcoke FOB prices - historical view 2007-22

Meanwhile, petcoke has stabilised with a high discount on current levels. Supply has increased but demand has declined. As a result, petcoke is now in the very cheap zone.

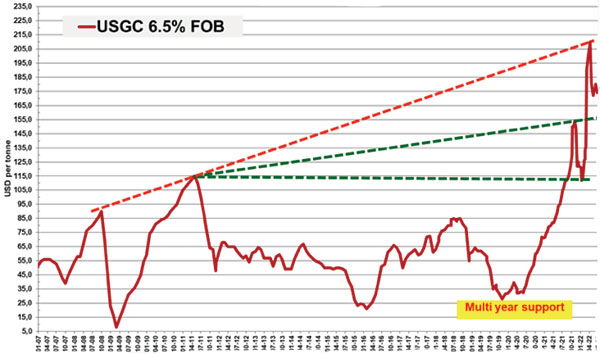

In terms of petcoke prices, the high-sulphur (6.5 per cent S) petcoke FOB contract is currently at US$174, with an expected trading range of US$170-190. Resistance is to be found at US$200, 215, 235 and 250, while support is around US$170, 155 and 115. Multiyear support is found at US$35.

High-sulphur petcoke (6.5%) 40HGI FOB USGC - historical view 2007-22

Discounts for high-sulphur petcoke when compared with API4 coal have increased when compared with previous energy report. The discount for 6.5 per cent S petcoke FOB sold at US$174 is at 54 per cent when compared with 3Q22 API4 coal sold at US$300. The CIF ARA 6.5 per cent S petcoke contract sold at US$201 is at a discount of 48 per cent, when compared with 3Q22 API2 coal sold at US$310.

Freight rates weakened considerably with USGC-ARA contracts falling to US$27.